Singapore - These are the research findings of the 48th round of the DBS-SKBI Singapore Index of Inflation Expectations (SInDEx) Survey at the Sim Kee Boon Institute for Financial Economics (SKBI), Singapore Management University (SMU).

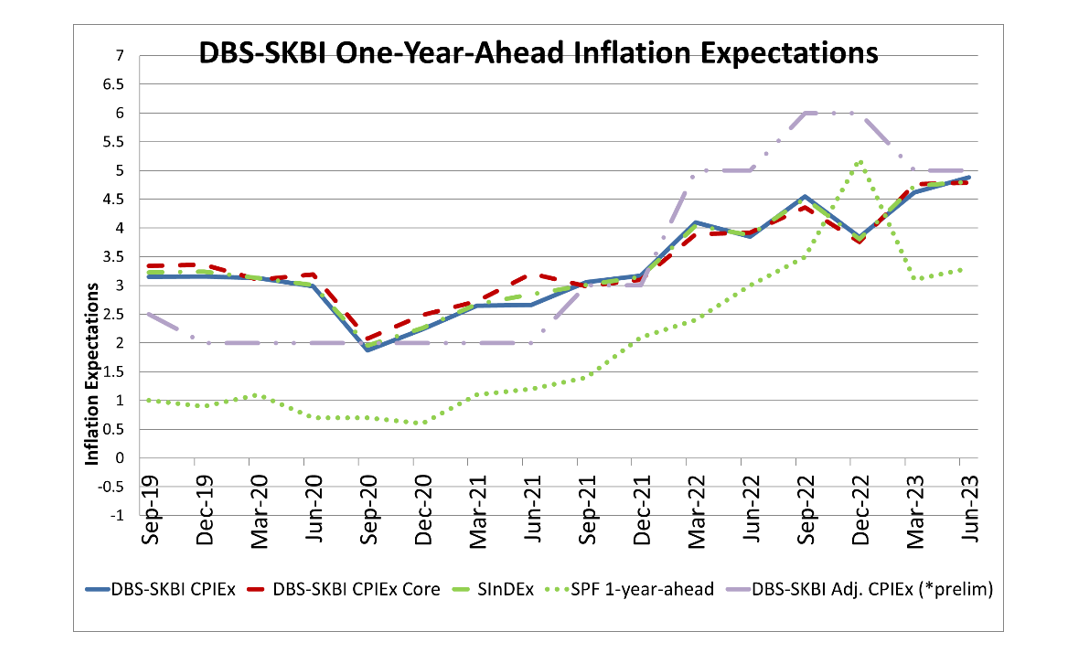

- One-year-Ahead headline inflation expectations rose to 4.9% in June 2023, from 4.6% in March 2023. There is a continuing but slowing trend of increase in inflation expectations that started in December 2022. Divergent signals emanating from the global macroeconomy, and from policymakers might be prompting variances in outlook in the perceptions of the consumers. On one hand, the reopening of all economies, including China, and the relaxation of global travel restrictions have boosted global demand. But there are headwinds, possibly cyclical, to global growth. These include an obdurately persistent cost-of-living crisis, tightening financial conditions and job markets in major economies, the entrenched Russia-Ukraine conflict, continuing geopolitical tensions in the world broadly bifurcated by Sino-US tensions, dampening the global outlook. The second quarter one-year-ahead inflation expectations continue to be higher than the average one-year-ahead headline inflation expectations of 3.3% since the inception of this index between 2012 and 2022.

- As a comparison benchmark, data from the Monetary Authority of Singapore Survey of Professional Forecasters (MAS SPF) released in June 2023 showed that the median forecasts of Consumer Price Index-All Items (CPI-All Items) inflation for 2023 was 5%, and the MAS Core inflation was 4.1%. This is in contrast to the figures of 3% and 4.1% for 2024, respectively. The latest CPI data release from the Department of Statistics showed that CPI-All Items rose by 5.8% in January-May 2023 period, compared with the same period in 2022, with the latest May 2023 monthly inflation print coming in at 5.1% year on year. On 14 April 2023, MAS maintained the rate of appreciation of the Singapore Dollar Nominal Effective Exchange Rate (S$NEER) policy band, following five consecutive tightening moves between October 2021 and October 2022. These moves have already tempered the momentum of inflation and their impact is still working through the economy. The current appreciating path of the S$NEER policy band will continue to reduce imported inflation and help curb domestic cost pressures.

- The overall Consumer Price Index (CPI) Inflation Expectations (CPIEx), after adjusting for potential component-wise behavioural biases and re-combining across components, inched up to 5.8% in June 2023 from 5.2% in March 2023. The One-year-ahead Inflation expectations of major components of CPI like Food (from 6%-7%), Transportation (from 5%-6%), Housing and Utilities (from 5%-6%) increased slightly while all other components, namely Healthcare, Education, Recreation & Culture, Clothes and Footwear, Household Durables and Services, Communications and Miscellaneous items including personal care, remained steady at 5% between the March 2023 and June 2023 surveys. Higher demand related to travel, food and beverage and accommodation without a commensurate increase in supply might have contributed to the slight increase in some inflation expectations.

- We also polled free response overall inflation expectations after accommodating for potential behavioural biases, and these remained unchanged at 5% between the surveys of March 2023 and June 2023. These free response polls help us to gauge perceptions of anchoring of inflation expectations and consumer sentiments in an aggregate sense.

- In the June 2023 wave, continuing from June 2022 survey, we took a more forward-looking approach to analyse the impact of global economic developments on Singapore’s economic growth and inflation. The findings are:

-

Overall, given the geopolitical unrest and uncertainty, financial sector volatility, continuation of tightening – albeit at a slower pace – of monetary policies by major economies, tight domestic job market and general cost-of-living pressures, Singaporean consumers expect Singapore’s economic growth to dampen slightly over the next 12 months.

-

Responding to overall cost impact on their pocketbook, Singaporean consumers also felt that their overall expenses would increase slightly over the next 12 months.

-

In June 2023, Singaporean consumers polled on how they feel the overall inflation scenario would unfold in the next 12 months seem to hold quite a divergent view. Around 51%, compared to 50% in March 2023, of those surveyed in June 2023 expect inflation to decline. On the other hand, 43% surveyed in June 2023, compared to 41% in March 2023, felt that it will increase.

-

The main reason cited by those expecting inflation to decline is a slowdown in global growth (41%). Central banks in major economies raising interest rates (40%) is given as the second most common reason cited. A distant third, 13% felt the resolution of pandemic-induced supply chain disruptions are also expected to relieve price pressures. Among respondents expecting inflation to increase over the next 12 months, the most common reasons cited were central banks in major economies raising interest rates (27%), followed by geopolitical uncertainties due to the Ukraine-Russia conflict (26%), supply chain disruptions (21%) and high demand due to easing of COVID-19 restrictions (20%).

-

In the June 2023 survey, current economic conditions have a limited negative impact on one-year-ahead and five-year-ahead overall inflation expectations on the views of the respondents. This slight negative impact expecting slightly increased inflation expectations was polled across components like Food, transportation, housing and utilities, and healthcare but there was no such discernible impact on education, recreation and culture, communications, clothes and footwear, household durables and services, and miscellaneous items including personal effects.

-

There was however some significant divergence among respondents regarding the impact on inflation expectations for most components, including Food, Transportation, Housing & utilities, Healthcare, Clothes & footwear, Household durables & services, Miscellaneous items including personal effects besides overall one-year and five-year ahead inflation expectations. We find distinct “bimodal” distributions, where there are two large groups who disagree whether the impact would be positive or negative, demonstrating a perception difference due to the global economic uncertainty.

-

-

Alberto Cavallo of Harvard Business School (Cavallo, 2020) and a report by the European Central Bank (Kouvavas et al., 2020) highlighted potential biases in CPI calculations with fixed baskets as respondents made substantive changes to their consumption baskets owing mainly to the pandemic. In the June 2023 survey, respondents expected to have limited increases in expenses for Food, Transportation, Housing & Utilities, Healthcare but no discernible changes in the other CPI components including Education, Recreation and Culture, Communication, Clothes and Footwear, Household durables and Services and Miscellaneous Personal Effects. These results indicate that respondents expect the consumption baskets to change, with higher spending on certain components over the next 12 months compared to other components, owing to possibly more permanent consumption changes post-pandemic relative to consumption and price patterns across the board.

- Excluding inflation expectations in accommodation and private transportation, the One-year-Ahead CPIEx core inflation expectations for this SInDEx survey in June 2023 remained unchanged at 4.8% compared to March 2023 survey. This is an early indication of prices stabilising and anchoring of inflation expectations without the more volatile and policy sensitive components.

- For a subgroup of the population who owns their accommodation and uses public transport, the One-year-Ahead CPIEx core inflation expectations elevated to 4.9% in June 2023 from 4.7% in March 2023, but the pace of increase in expectations remained broadly on a moderating path compared to the highs in 2021-22. This sub-sample measurement is potentially more representative than the full sample measurement, due to high home ownership and public transport ridership in Singapore.

- Unlike the fixed response which might be susceptible to various behavioural biases, core CPIEx Inflation Expectations (excluding accommodation and private road transportation expenses), after adjusting for potential component-wise behavioural biases and re-combining across components, increased to 5.8% in June 2023 from 5.3% in March 2023 survey. The free response core CPIEx Inflation Expectations however stayed unchanged at 5% in June 2023 compared to March 2023 survey, corroborating the early slowing trend in inflation expectations.

-

The One-year-Ahead composite index SInDEx1 that puts less weight on more volatile components like accommodation, private road transport, food and energy-related expenses polled at 4.8% in June 2023, inching up slightly from 4.7% in March 2023. It nonetheless continues to be higher than the second quarter average of 3.3% since the survey’s inception from 2012 till 2022.

-

In addition, in June 2023, around 11.2% of Singaporeans polled expect a salary reduction of more than 5.0% in the next 12 months compared to 9.8% of respondents in March 2023. The expectation of a median salary increment of between 1% and 5% remained unchanged compared to the March 2023 survey.

Figure 1: One-year-Ahead inflation expectations: The chart shows the quarterly DBS-SKBI CPIEx (CPI-All Item) and DBS-SKBI CPIEx Core (Excluding accommodation and private road transportation components) One-Year-Ahead Inflation Expectations polled in the quarterly online Singapore Index of Inflation Expectations (SInDEx) Survey conducted on a representative sample of Singaporean residents between 19 June and27 June 2023. (Source: SKBI, SMU, MAS, Department of Statistics)

DBS Chief Economist and Managing Director of Group Research, Dr Taimur Baig, commented, “After nearly two years of inflation dominating the macro landscape, the global price picture has finally become somewhat benign. Commodity prices have softened, food inflation is moderate, electronics prices are correcting due to demand contraction, and companies are beginning to scale back price increase strategies. Singapore’s consumers will be seeing these developments reflected in their pocketbooks during the second half of this year, which would be a source of relief after a few years of relentless inflation. As such developments take hold, inflation expectations would adjust as well, particularly in the presence of lacklustre demand outlook in the region.”

SMU Assistant Professor of Finance and Founding Principal Investigator of the Quarterly DBS-SKBI SInDEx Project, Aurobindo Ghosh, highlighted, “The World Bank Group summarised the ‘precarious’ state of the global economy in its June 2023 Global Economic Prospects citing overlapping economic shocks. These are precipitated by the ongoing geopolitical conflicts and tensions, tightening of monetary policy to contain runaway inflation, restrictive credit conditions due to recent banking sector stress, with warnings of slowdown in global growth in 2023 and a lingering weakness in 2024. A small open trade-based economy like Singapore is susceptible to these global headwinds and has to walk a fine line between controlling cost of living and catalysing growth.”

He added that domestically, ongoing, and planned increases in GST and other pass-through costs like transportation, rental and higher wages due to a tighter labour market, besides the slowdown in the growth of major trading partners like China, might also dampen Singapore demand. He observed: “Singaporean consumers, being aware of these challenges, seem to believe that there would be some tempering of the trend of inflation, particularly in areas without the more volatile policy-sensitive elements like transportation and housing, indicating some initial signs of anchoring of medium-term inflation expectations despite the global uncertainty.”

The DBS-SKBI SInDEx Inflation Expectations survey, he shared, is designed to be robust in monitoring expectations of inflation.

He said: “Recent academic literature has highlighted certain behavioural biases creep into responses of those who are exposed to more volatile grocery and gasoline prices when asked about subjective inflation expectations (Weber et al., 2022). However, it has been established that survey-based inflation expectations of professionals, households and consumers are instrumental in forecasting future inflation (Ang et al., 2007).”

Since 2018, the survey has accommodated some of the behavioural biases by cross referencing multiple choice based and free response options.

He noted that opinions seem to show a clear dichotomy, with one group expecting inflation to pare down while other expecting inflation rate to rise. “This can be reconciled, as it is also well known that any monetary policy tightening takes effect over a period of time, so we have to investigate the gradual changes to trends in inflation expectations to measure the effectiveness or anchoring of inflation expectation in a small open economy like Singapore that runs an exchange rate based monetary policy,” Dr Ghosh observed.

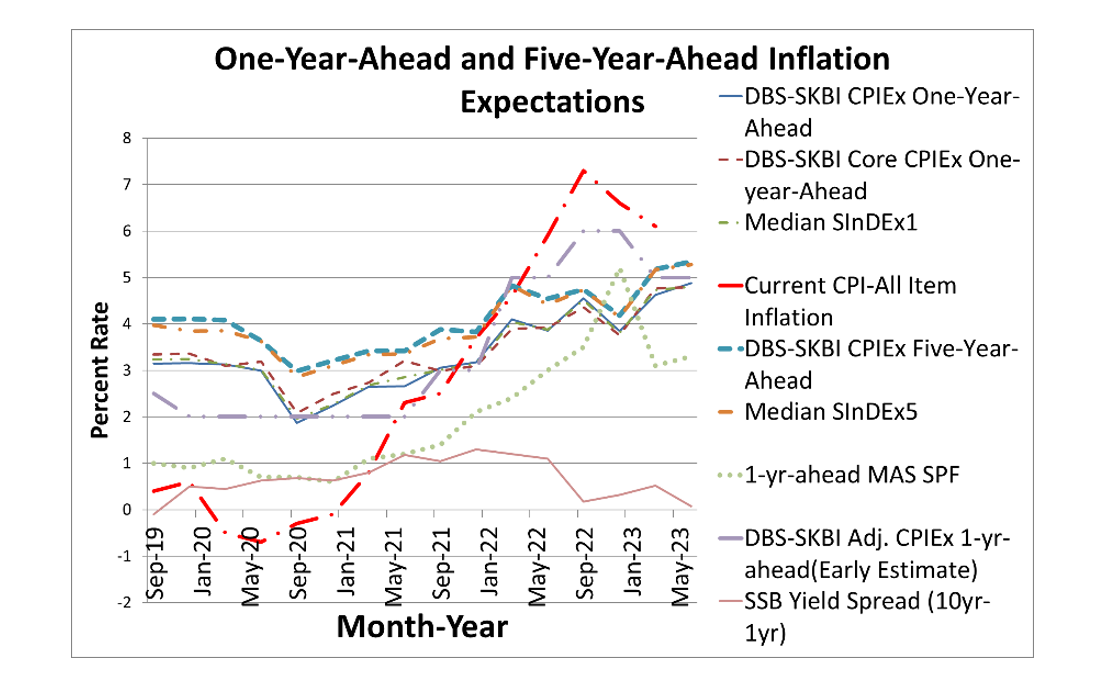

For the longer horizon, the Five-year-Ahead CPIEx inflation expectations rose slightly to 5.3% in June 2023 from 5.2% in March 2023. The current polled number continues to be higher than the first quarter average of 4.1% since the survey’s inception in 2012.

The Five-year-Ahead CPIEx core inflation expectations (excluding accommodation and private road transportation related costs) however remained unchanged at 5.2% in June 2023 compared to March 2023. Overall, the composite Five-year-Ahead SInDEx5 also increased slightly to 5.3% in June 2023 from 5.2% in March 2023. In comparison, the first quarter average value (since the survey’s inception in 2012 till 2022) of the composite Five-year-Ahead SInDEx5 is 4.0%.

After adjusting for potential behavioural biases, the free response Five-Year-Ahead Headline Inflation Expectations increased to 7% in June 2023 compared to 5% March 2023, while the free response Core Five-Year-Ahead Inflation Expectations also increased to 7% in June 2023 from 6% in March 2023. This might be reflecting some dampening of consumer confidence due to concern over cost-of-living increases.

“Slowdown or flattening in the trend of medium- and long-term inflation expectations bodes well for both consumer confidence as well as impact of global economic uncertainty on cost of living. Policymakers around the world seem to be studying data to finetune their policy stance and be cautiously optimistic about early signs of slowing inflation to avoid precipitating a ‘hard-landing’ of economic recession,” Asst Prof Ghosh commented.

References:

Ang, A., G. Bekaert, and M. Wei., 2007, “Do Macro Variables, Asset Markets, or Surveys Forecast Inflation Better?” Journal of Monetary Economics, 54:4, pp. 1163–212.

Cavallo, A., 2020, "Inflation with COVID Consumption Baskets." NBER Working Paper Series, No. 27352, June 2020 (Harvard Business School Working Paper, No. 20-124, May 2020). (https://www.hbs.edu/faculty/Pages/item.aspx?num=58253, accessed on July 14, 2020)

Kouvavas, O., R. Trezzi, M. Eiglsperger, B. Goldhammer and E. Goncalves, 2020, “Consumption patterns and inflation measurement issues during the COVID-19 pandemic,” ECB Economic Bulletin, Issue 7/2020. (https://www.ecb.europa.eu/pub/economic-bulletin/html/eb202007.en.html#toc6, accessed on July 14, 2020)

Weber, M., F. D’Acunto, Y. Gorodnichenko and O. Coibion, 2022, “The Subjective Inflation Expectations of Households and Firms: Measurement, Determinants, and Implications,” Journal of Economic Perspectives, 36:3, pp. 157–184.

Methodology

DBS-SKBI SInDEx survey yields CPIEx Inflation Expectations (estimating headline inflation expectations) and related indices are products of the online quarterly survey of around 500 randomly selected individuals representing a cross section of Singaporean households. The survey is led by Principal Investigator Dr. Aurobindo Ghosh, Assistant Professor of Finance (Education) at Lee Kong Chian School of Business, SMU. The online survey, powered by Agility Research and Strategy, helps researchers understand the behavior and sentiments of decision makers in Singaporean households. DBS Group Research is a co-sponsor and research partner with the Sim Kee Boon Institute for Financial Economics (SKBI) at SMU.

The quarterly DBS-SKBI SInDEx survey has also yielded two composite indices, SInDEx1 and SInDEx5. SInDEx1 and SInDEx5 measure the One-year inflation expectations and the Five-year inflation expectations, respectively. The sampling was done using a quota sample over gender, age and residency status to ensure representativeness of the sample. Employees in some sectors like journalism and marketing were excluded as that might have an effect on their responses to questions on consumption behavior and expectations.

The DBS-SKBI SInDEx survey was augmented in June 2018, based on a joint research study conducted by SMU researchers in collaboration with MAS and the Behavioural Insights Team, where respondents were polled on their perceptions of components of the Consumers Price Index (CPI) and adjusted for possible behavioural biases prevalent in online surveys.

Based on the recommendations of the joint study, since March 2019 the research team has polled the One-year-Ahead inflation expectations of all of the major components of CPI-All Items inflation. For June 2023 survey, DBS-SKBI CPIEx headline inflation expectations indices increased compared to March 2023, while the core inflation expectations remained largely unchanged. Further, the behaviourally adjusted component-wise and recombined inflation expectations, causing the overall behaviourally adjusted indices increased slightly though at a slower pace. In free response answers, compared to March 2023 survey, respondents in the June 2023 survey polled One-year-Ahead Headline and Core Inflation Expectations remained unchanged as a positive sign of anchoring. Overall, the results indicate a slowdown in the trend of medium and long inflation expectations.

We introduced a new ratio in the June 2020 survey, on the life versus livelihood debate as an aftermath of the Covid 19 pandemic - the ratio of respondents who feels livelihood should be prioritised over life vis-à-vis those who feel the other way. This ratio increased to 3.6 in June 2023 compared to 3 in March 2023. For every respondent who prioritised life over livelihood, there were about 4 who prioritised livelihood over life, signaling life returning to normal with an endemic Covid-19.

Figure 2: Five-year-Ahead-Inflation Expectations in Singapore: The chart shows the quarterly DBS-SKBI CPIEx (CPI-All Item), DBS-SKBI CPIEx Core (excluding accommodation and private road transportation components), SInDEx (Composite index with lower weights on volatile components like food, energy, accommodation and private road transportation) One-Year and Five-Year-Ahead Inflation Expectations polled online quarterly for the Singapore Index of Inflation Expectations (SInDex) Survey conducted from 19 June to 27 June, 2023. The chart shows a preliminary estimate of Behaviourally Adjusted One-year-Ahead overall DBS-SKBI Adjusted CPIEx. As comparison benchmarks, the chart provides the most recent quarterly CPI-All Item Inflation, MAS Survey of Professional Forecasters median One-year-Ahead CPI-All Item inflation forecasts and the yield spread of 10-year and 1-year Singapore Savings Bonds (SSB). (Source: SKBI, SMU, MAS, Department of Statistics)

About DBS

DBS is a leading financial services group in Asia, with over 280 branches across 18 markets. Headquartered and listed in Singapore, DBS has a growing presence in the three key Asian axes of growth: Greater China, Southeast Asia and South Asia. The bank's "AA-" and "Aa1" credit ratings are among the highest in the world.

Recognised for its global leadership, DBS has been named “Best Bank in the World” by Global Finance. The bank is at the forefront of leveraging digital technology to shape the future of banking, having been named “World’s Best Digital Bank” by Euromoney. In addition, DBS has been accorded the “Safest Bank in Asia” award by Global Finance for ten consecutive years from 2009.

DBS provides a full range of services in consumer, SME and corporate banking. As a bank born and bred in Asia, DBS understands the intricacies of doing business in the region’s most dynamic markets. DBS is committed to building lasting relationships with customers, and positively impacting communities through supporting social enterprises, as it banks the Asian way. It has also established a SGD 50 million foundation to strengthen its corporate social responsibility efforts in Singapore and across Asia.

With its extensive network of operations in Asia and emphasis on engaging and empowering its staff, DBS presents exciting career opportunities. The bank acknowledges the passion, commitment and can-do spirit in all of our 26,000 staff, representing over 40 nationalities. For more information, please visit www.dbs.com.

About Singapore Management University

Established in 2000, Singapore Management University (SMU) is recognised for its disciplinary and multidisciplinary research that address issues of global relevance, impacting business, government, and society. Its distinctive education, incorporating innovative experiential learning, aims to nurture global citizens, entrepreneurs and change agents. With more than 12,000 students, SMU offers a wide range of bachelors, masters and PhD degree programmes in the disciplinary areas associated with six of its eight schools - Accountancy, Business, Economics, Computing, Law and Social Sciences. Its seventh school, the SMU College of Integrative Studies, offers a bachelor’s degree programme in deep, integrative interdisciplinary education. The College of Graduate Research Studies, SMU’s eighth school, enhances integration and interdisciplinarity across the various SMU postgraduate research programmes that will enable our students to gain a holistic learning experience and well-grounded approach to their research. SMU also offers a growing number of executive development and continuing education programmes. Through its city campus, SMU focuses on making meaningful impact on Singapore and beyond through its partnerships with industry, policy makers and academic institutions. For more information, please visit www.smu.edu.sg

About Sim Kee Boon Institute for Financial Economics

The Sim Kee Boon Institute for Financial Economics (SKBI) is the premier Asian institute for applied financial research and training in financial economics. It is the think-tank within SMU that spearheads cutting-edge research in financial markets that is driven by industry and societal needs in Singapore and the region.

Over the last 10 years, a diverse portfolio of financial research, outreach and training initiatives has been built. In the coming 10 years, while further expanding that traditional financial economics portfolio, the Institute will focus our efforts on the areas of financial inclusion and literacy, sustainable finance, financial technology, and data and governance. To maintain our relevance to finance practitioners and policy-makers, SKBI also adopts a view on Asian and global economic trends.

Supported by SMU faculty and in collaboration and partnership with industry experts, relevant government bodies, and other world-renowned research agencies, the Institute conducts fundamental and applied research which aims at solving real-world issues. Besides research, SKBI also actively engages in outreach, executive training and research dissemination through organising courses, seminars and conferences. Our purpose-oriented activities are designed to bridge the gap between theory and practice and to act as accelerators with regard to financial policies and regulations. SKBI is led by an Advisory Board that consists of prominent leaders of local and international organisations in the finance industry that have footprints across Asia, and of government agencies.

[End]