SMU’s Lee Kong Chian School of Business, in collaboration with DBS Group Research and partly funded by DBS, released the Singapore Index of Inflation Expectations survey on 20 January 2026 which showed that the majority of Singaporeans expect headline inflation to rise slightly in 2026 as a result of global high trade policies followed by geopolitical uncertainties, higher interest rates, supply chain disruptions, and fiscal responsibility measures, such as higher value-added taxes. #SInDEx

SMU’s Lee Kong Chian School of Business, in collaboration with DBS Group Research and partly funded by DBS, released the Singapore Index of Inflation Expectations survey on 20 January 2026 which showed that the majority of Singaporeans expect headline inflation to rise slightly in 2026 as a result of global high trade policies followed by geopolitical uncertainties, higher interest rates, supply chain disruptions, and fiscal responsibility measures, such as higher value-added taxes.

SMU’s Lee Kong Chian School of Business, in collaboration with DBS Group Research and partly funded by DBS, released the Singapore Index of Inflation Expectations survey on 20 January 2026 which showed that the majority of Singaporeans expect headline inflation to rise slightly in 2026 as a result of global high trade policies followed by geopolitical uncertainties, higher interest rates, supply chain disruptions, and fiscal responsibility measures, such as higher value-added taxes. Commenting on the survey result, SMU Assistant Professor of Finance (Education) Aurobindo Ghosh said that this comes as policy uncertainty remained elevated throughout 2025. Asst Prof Ghosh said that the global economy and the equity market, has been surprisingly resilient despite the onslaught of conflicts, tariffs and disruptions. Against this backdrop, he added that consumers in Singapore, as part of a small open economy, weighed in their opinion that overall inflation (would) be slightly higher across the board in the medium term.

SMU’s Lee Kong Chian School of Business, in collaboration with DBS Group Research and partly funded by DBS, released the Singapore Index of Inflation Expectations survey on 20 January 2026 which showed that the majority of Singaporeans expect headline inflation to rise slightly in 2026 as a result of global high trade policies followed by geopolitical uncertainties, higher interest rates, supply chain disruptions, and fiscal responsibility measures, such as higher value-added taxes. Commenting on the survey result, SMU Assistant Professor of Finance (Education) Aurobindo Ghosh said that this comes as policy uncertainty remained elevated throughout 2025. Asst Prof Ghosh said that the global economy and the equity market, has been surprisingly resilient despite the onslaught of conflicts, tariffs and disruptions. Against this backdrop, he added that consumers in Singapore, as part of a small open economy, weighed in their opinion that overall inflation (would) be slightly higher across the board in the medium term.

SMU’s Lee Kong Chian School of Business, in collaboration with DBS Group Research and partly funded by DBS, released the Singapore Index of Inflation Expectations survey on 20 January 2026 which showed that the majority of Singaporeans expect headline inflation to rise slightly in 2026 as a result of global high trade policies followed by geopolitical uncertainties, higher interest rates, supply chain disruptions, and fiscal responsibility measures, such as higher value-added taxes. Commenting on the survey result, SMU Assistant Professor of Finance (Education) Aurobindo Ghosh said that this comes as policy uncertainty remained elevated throughout 2025. Asst Prof Ghosh said that the global economy and the equity market, has been surprisingly resilient despite the onslaught of conflicts, tariffs and disruptions. Against this backdrop, he added that consumers in Singapore, as part of a small open economy, weighed in their opinion that overall inflation (would) be slightly higher across the board in the medium term.

SINGAPORE, 22 April 2026 (Wednesday) - These are the research findings of the 59thround of the DBS-SKBI Singapore Index of Inflation Expectations (SInDEx) Survey at the Sim Kee Boon Institute for Financial Economics (SKBI), Singapore Management University (SMU),conducted between 25 March and 1 April 2026.

In the March 2026 survey, a large majority — 88.3% of those surveyed — believe that inflation will rise over the medium term or next one year, up from 83.4% in December. Only 5% of Singaporeans polled think that inflation will go down in the next year, which is a slight drop from 6% in December 2025. The results of this quarterly online survey suggest that many expect inflation to increase in the next year, due mainly to global trade policies and rising fuel prices.

In March 2026, for the respondents expecting inflation to increase over the next 12 months, the most common reason cited was geopolitical uncertainties and the conflicts involving Hamas and Israel, Ukraine and Russia, and Iran and Israel (64%). This is followed by supply chain disruptions (13.3%) and higher trade policy uncertainty, like tariffs (9%). Those expecting inflation to decline cited the uncertain impact of the resolution of supply chain disruptions (28%), followed by central banks keeping interest rates high (20%), as well as slowdown in global growth (20%). These reasons are followed by more competition leading to lower prices (16%).

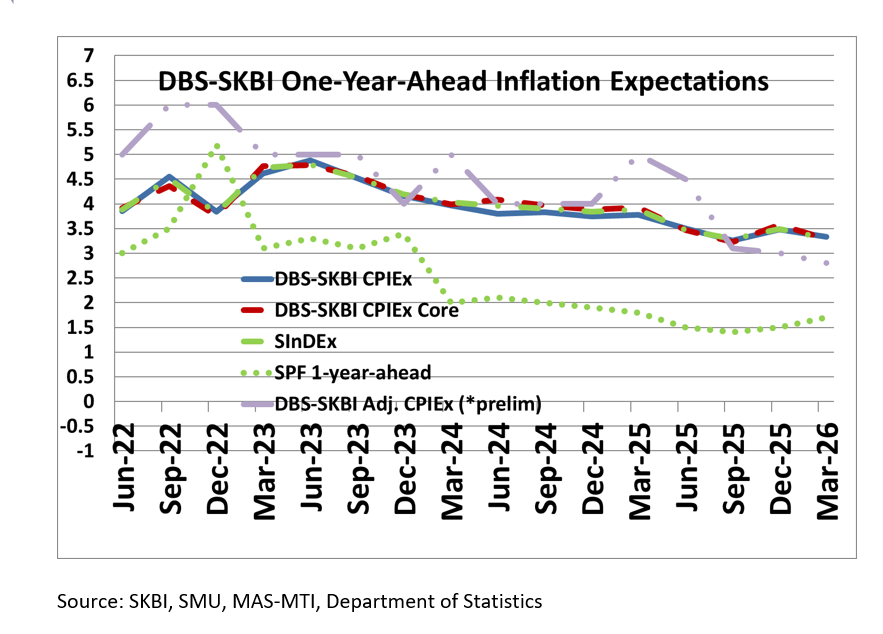

Despite the majority opinion, One-year-Ahead headline inflation expectations pared to 3.3% in March 2026 from 3.5% in December 2025 on average. The first quarter One-year-Ahead inflation expectations were slightly below the average first quarter One-year-Ahead headline inflation expectations of 3.5% recorded since the inception of this index in the third quarter of 2011.

As a comparison, data from the Monetary Authority of Singapore’s Survey of Professional Forecasters (MAS SPF) released in March 2026 (based on February 2026 data) showed that the median forecast of the Consumer Price Index (CPI)-All Items inflation for 2026 (quarterly) was 1.5% (1.7% for 2027), while MAS Core Inflation median forecast was 1.5% (1.7% for 2027) (MAS SPF March 2026, Table A.4 and Table A.6). The latest CPI data released by the Department of Statistics (DOS) showed that CPI-All Items rose by 1.3% between January and February 2026, compared to the same period in 2025. The latest February 2026 monthly headline or all item inflation print came at 1.2% year-on-year, while the MAS Core Inflation Measure was 1.4% (DOS CPI, March 2026). The base year was changed to 2024 with the adjustment of the consumption baskets based on the Household Expenditure Survey 2023. In their first two quarterly reviews of 2025, MAS reduced the rate of appreciation of the Singapore Dollar Nominal Effective Exchange Rate (S$NEER) policy band slightly, implementing two consecutive loosening moves after having kept the policy stance unchanged since October 2022. In April 2026, MAS tightened monetary policy by slightly increasing the slope of the S$NEER policy band, in response to higher projected inflation driven mainly by imported cost pressures (MAS Monetary Policy Statements, July and October 2025, April 2026). The next monetary policy statement will be released by July 2026.

The overall aggregated Consumer Price Index Inflation Expectations, re-combining across components after addressing potential component-wise behavioural biases, declined from 3.1% in December 2025 to 3% in March 2026. One-year-Ahead inflation expectations of major components of CPI held unchanged in most of the components, namely Food (unchanged at 3%), Housing & Utilities (unchanged at 3%), Healthcare (unchanged at 4%), Information and Communications (unchanged at 2.2%) and Miscellaneous Goods & Services including Personal Care (unchanged at 3%) while there was a slight decline in Education (3% to 2.8%), Household Durables & Services (3% to 2.9%), Recreation, Sport & Culture (3% to 2%), Clothing & Footwear (3% to 2%). In contrast, inflation expectations increased for Transportation (3% to 3.5%). Flattening or decline in inflation expectations across most categories, except for direct oil price-related components like transportation, signals consumers expect price increases to be muted over the next 12 months.

The survey team also polled free-response overall inflation expectations, after reducing potential behavioural biases by informing respondents of current aggregated economic data. The team found that the One-year-Ahead headline inflation expectations pared down from 3% in December 2025 to 2.8% in March 2026. These free-response polls help us gauge perceptions of the anchoring of inflation expectations and consumer sentiments in an aggregated sense, after accommodating changes in respondents’ personal consumption expenditure.

In the March 2026 survey, continuing since June 2022, we took a more forward-looking approach in analysing the impact of global economic developments on Singapore’s economic growth and inflation.

Overall, in response to increased geopolitical uncertainties and fragilities in the global order, including ongoing and emerging conflicts, and strategic policy uncertainty affecting global trade, Singaporean consumers surveyed in March 2026 expected a slight negative impact on the country’s economic growth over the next 12 months.

In addition, Singaporean consumers also opined in the March 2026 survey that over the next 12 months, their overall expenses are expected to increase slightly. Nonetheless, in response to new questions added since the September 2025 survey, respondents believe that their household situation is expected to remain unchanged economically and financially in the next 12 months. They also opined that they expect a slight negative impact on business conditions in the next 12 months, compared to last year. Respondents also found conditions for buying bigger ticket items like household appliances or furniture are expected to slightly worsen in the next 12 months. Over the next five years business situations are expected to be occasionally challenging. All these responses indicate stable consumer and business sentiment over the last quarter, although there are signs of slightly worsening expectations.

In the March 2026 survey, respondents opined that under current economic conditions, they expect only a slight increase in the One-year-Ahead rate. However, the respondents expect a moderate increase in Five-year-Ahead overall inflation expectations. Because of geopolitical conditions, respondents expect inflation to increase slightly for components like Food, Transport, Housing & Utilities, Healthcare, Education, Household Durables & Services, Recreation, Sport & Culture, Information & Communication, Clothing & Footwear, and Miscellaneous Goods & Services.

Alberto Cavallo of Harvard Business School (Cavallo, 2020) and European Central Bank (Kouvavas et al., 2020) highlighted potential biases in CPI calculations with fixed baskets as respondents made substantive changes to their consumption baskets owing mainly to the COVID-19 pandemic. In the March 2026 survey, Singaporean consumers opined that in the next 12 months, they expect no change in the budget share of Food, Transport, Housing and Utilities, Healthcare costs, Household Durables & Services, Education, Recreation, Sport & Culture, Clothes & Footwear, Information & Communications and Miscellaneous Goods & Services. Also, since early 2025 the base year was changed to 2024 with the adjustment of the consumption baskets to consider the Household Expenditure Survey 2023. The latter is repeated every five years.

Excluding the volatile components of Accommodation and Private Transportation, the One-year-Ahead CPIEx core inflation expectations dropped to 3.3% in March 2026 compared to 3.6% in December 2025. For a subgroup of the population who owns their accommodation and uses public transport, the One-year-Ahead CPIEx core inflation expectations also pared to 3.3% in March 2026 from 3.6% in December survey, corroborating the findings. This sub-sample measurement is potentially more representative and hence more accurate than the full sample measurement, due to high home ownership and public transport ridership in Singapore.

Unlike the fixed radio-button response, which might be susceptible to various behavioural biases, the free-response core CPIEx Inflation Expectations (excluding Accommodation and Private Transportation expenses) however remained more stable. After adjusting for potential component-wise behavioural biases and re-combining across components, the core-CPIEx Inflation Expectations (excluding Accommodation and Private Transportation expenses) pared to 2.9% in March 2026 compared to 3.1% in December 2025. The free-response core CPIEx remained unchanged at 3% in March 2026 compared to December 2025. The slightly higher inflation expectations obtained from the fixed response (radio button) compared to the behaviourally adjusted free response suggest that there are still some cognitive biases in the fixed response that can be partially offset by the behaviourally adjusted methods.

The One-year-Ahead composite index SInDEx1 that puts less weight on more volatile components like Accommodation, Private Road Transport, Food and Energy-related expenses also dropped to 3.3% in March 2026 compared to 3.5% in December 2025. It is slightly lower than the first quarter’s average of 3.5% since the inception of the survey in September 2011.

In addition, about 6.9% of respondents in March 2026 expect more than a 10% reduction in salary in the next 12 months, compared to 5.9% in the December 2025 survey. The expectation of median salary increments in March 2026 of between 1-5% remained unchanged, compared to December 2025 survey.

Figure 1: One-year-Ahead inflation expectations: The chart shows the quarterly DBS-SKBI CPIEx (CPI-All Item) and DBS-SKBI CPIEx Core (Excluding Accommodation and Private Transportation components) One-year-Ahead Inflation Expectations, polled in the quarterly online Singapore Index of Inflation Expectations (SInDEx) Survey. The latest round was conducted on a representative sample of Singaporean residents between 25 March and 1 April 2026. (Source: SKBI, SMU, MAS-MTI, Department of Statistics)

DBS Bank Chief Economist and Managing Director of Group Research, Dr Taimur Baig commented, “Energy shock is permeating through the global economy. With pump prices rising, and other energy-related pressure points in the pipeline, hits to consumer and business sentiment are inevitable. We expect the recent bump in inflation expectations to be modest, given the proactive way the supply chain is being managed by the authorities and monetary policy measures, recent and forthcoming, by MAS.”

Dr Aurobindo Ghosh, Assistant Professor of Finance at Singapore Management University (SMU), the creator and founding Principal Investigator of the Quarterly DBS-SKBI SInDEx Project, observed, “In April 2026, International Monetary Fund (IMF) in their semi-annual World Economic Outlook (WEO) revised their 2026 global growth forecast to 3.1% from 3.3% they projected in January 2026, besides increasing their global inflation forecasts. The US-Israel conflict with Iran and the ensuing retaliatory closure of the Strait of Hormuz, which accounts for about 20% of global oil and natural gas shipments is of particular concern. The potential of a lingering crunch in supply and the surge in commodity prices like oil, natural gas, byproducts of the petrochemical industry like fertilisers and helium, poses a clear and present threat to the surge in inflationary pressures globally. While negotiations are ongoing to resolve the crisis, and showing positive signs for the continuous opening of the Strait of Hormuz as the fragile ceasefire takes shape, central banks around the world, including the MAS, are keeping a close watch. In a preemptive move, MAS announced a tightening of Monetary Policy in its April 2026 meeting, for the first time since October 2022.”

“From the DBS-SKBI SInDEx March 2026 survey, respondents seem to have more anchored inflation expectations overall though there are some differences of opinion. We gather some salient insights from the findings. First, on average, an overwhelming majority of about 88.3% believe that One-year-Ahead inflation expectations will be raised slightly, compared to only 5% who opined that One-year-Ahead inflation expectations will subside. Although the online survey might suffer from some behavioural bias like the Recency or Availability Bias overemphasising recent events, the main reasons cited are mainly geopolitical instability due to Ukraine-Russia, Hamas-Israel and Iran-US-Israel conflicts. This is followed by supply chain disruptions and trade policy uncertainty arising mainly from trade tariffs. Second, even after accommodating behavioural biases, we found that overall and component-wise inflation expectations seem to be holding steady or dipping slightly except transportation which is directly related to oil price appreciation (Clark, Ghosh and Hanes, 2018). This seems to suggest respondents have evaluated both the short-term price pressures due to ongoing conflicts but also are mindful that lingering conflict might mute longer term growth forecasts. Third, with the change of base of the Consumer Price Index (CPI) to 2024 and consumption baskets based on the 2023 Household Expenditure Survey (HES 2023), respondents opined that their consumption basket remained largely unchanged (Cavallo, 2020, Kouvavas et. al.,2020, Weber et. al., 2022). Finally, despite expecting to pay slightly more, respondents expect their spending will increase slightly over next 12 months. Over the next 12 months respondents believe that their household's overall economic and financial situation will remain unchanged. However, general business environment, job outlook as well as prospects of buying big ticket items are expected to slightly worsen in the next 12 months compared to the previous year. Over the next five years business conditions are also likely to worsen slightly according to respondents,” Dr Ghosh noted.

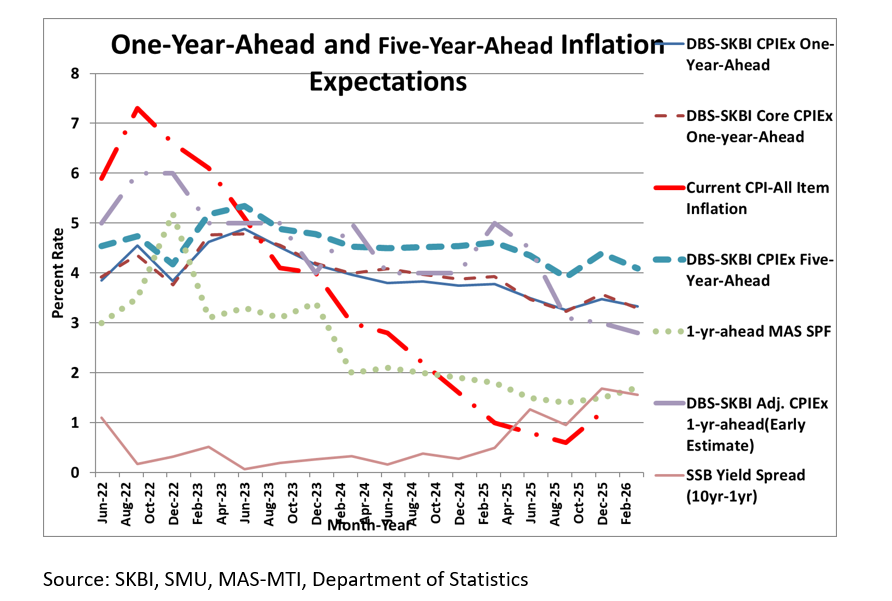

For the longer horizon, the Five-year-Ahead CPIEx inflation expectations dipped 4.4% in December 2025 to 4.1% in March 2026 – slightly below the first-quarter average of 4.3% polled since the survey’s inception in September 2011.

The Five-year-Ahead CPIEx core inflation expectations (excluding costs related to Accommodation and Private Transportation) also declined from 4.2% in December 2025 to 3.8% in March 2026. Overall, the composite Five-year-Ahead SInDEx5 also reduced from 4.2% in December 2025 to 4 in March 2026. In comparison, the first-quarter average value of the composite Five-year-Ahead SInDEx5 is 4.2%, since the survey’s inception in September 2011.

After adjusting for potential behavioural biases, the free-response Five-year-Ahead Headline Inflation Expectations dropped to 3.5% in March 2026 from 4% in December 2025. Five-year-Ahead Singapore Core Inflation Expectations also pared to 3.7% in March 2026 from 4% in December 2025.

Dr Aurobindo Ghosh added, “In March 2026, SInDEx survey indicated that long-term inflation expectations for the Five-year-Ahead Headline and the Five Year Ahead Singapore Core Inflation Expectations both dropped for respondents. After adjusting for potential behavioural biases, the long-term headline inflation expectations dropped below 4%. Despite short-term fluctuations due to US-Israel-Iran conflict, policy uncertainty on trade, this reflects some element of anchoring of longer-term inflation expectations and corroborates the importance and accuracy of survey-based measures (Ang, Baekert and Wei, 2007). The results of this survey indicate that, although there are potential risks on the horizon, Singapore is currently not facing an immediate threat of stagflation, which is characterised by high inflation coupled with stagnant economic growth or even contraction. Consumers feel that for the time being, the economy is managing to avoid the challenges associated with this adverse scenario, but it is necessary to monitor any inflationary trends and overall economic performance.”

Methodology

DBS-SKBI SInDEx survey yields CPIEx Inflation Expectations (estimating headline inflation expectations) and related indices are products of the online quarterly survey of around 500 randomly selected individuals representing a cross section of Singaporean households. The survey is led by Principal Investigator Dr Aurobindo Ghosh, Assistant Professor of Finance (Education) at Lee Kong Chian School of Business of the Singapore management University. The online survey, administered by YouGov, helps researchers understand the behaviour and sentiments of decision makers in Singaporean households. DBS Group Research is a co-sponsor and research partner with the Sim Kee Boon Institute for Financial Economics (SKBI) at SMU.

The quarterly DBS-SKBI SInDEx survey has also yielded two composite indices, SInDEx1 and SInDEx5. SInDEx1 and SInDEx5 measure the One-year inflation expectations and the Five-year inflation expectations, respectively. The sampling was done using a quota sample over gender, age and residency status to ensure representativeness of the sample. Employees in some sectors like journalism and marketing were excluded as that might have an effect on their responses to questions on consumption behaviour and expectations.

The DBS-SKBI SInDEx survey was augmented in June 2018, based on a joint research study conducted by SMU researchers in collaboration with MAS and the Behavioural Insights Team, where respondents were polled on their perceptions of components of the Consumers Price Index (CPI) and adjusted for possible behavioural biases prevalent in online surveys.

Based on the recommendations of the joint study, since March 2019 the research team has polled the One-year-Ahead inflation expectations of all of the major components of CPI-All Items inflation. For the March 2026 survey, DBS-SKBI CPIEx One-year-Ahead headline inflation expectations indices declined from December 2025. The core inflation expectations also pared in March 2026 compared December 2025. However, the behaviourally adjusted component-wise and recombined inflation expectations held steady or dropped slightly in March 2026 compared to December 2025, except for Transportation component which showed a slight increase. In free-response answers, compared to December 2025 survey, responses in the March 2026 survey polled for One-year-Ahead Headline and Singapore Core declined or held steady. Overall, the results indicate for both medium-term (One-year-Ahead) and long-term (Five-year-Ahead), inflation expectations declined slightly but it seems to attenuate when adjusted for behavioural bias.

Figure 2: Five-year-Ahead-Inflation Expectations in Singapore: The chart shows the quarterly DBS-SKBI CPIEx (CPI-All Item), DBS-SKBI CPIEx Core (excluding Accommodation and Private Road Transportation components), SInDEx (Composite index with lower weights on volatile components like Food, Energy, Accommodation and Private Transportation) One-year and Five-year-Ahead Inflation Expectations polled online quarterly for the Singapore Index of Inflation Expectations (SInDEx) Survey conducted from 25 March to 1 April 2026. The chart shows a preliminary estimate of Behaviourally Adjusted One-year-Ahead overall DBS-SKBI Adjusted CPIEx. As comparison benchmarks, the chart provides the most recent quarterly CPI-All Items Inflation, MAS Survey of Professional Forecasters median One-year-Ahead CPI-All Items inflation forecasts and the yield spread of 10-year and 1-year Singapore Savings Bonds (SSB). (Source: SKBI, SMU, MAS-MTI, Department of Statistics)

References:

Ang, A., G. Bekaert, and M. Wei., 2007, “Do Macro Variables, Asset Markets, or Surveys Forecast Inflation Better?” Journal of Monetary Economics, 54:4, pp. 1163–212.

Cavallo, A., 2020, "Inflation with COVID Consumption Baskets." NBER Working Paper Series, No. 27352, June 2020 (Harvard Business School Working Paper, No. 20-124, May 2020).(https://www.hbs.edu/faculty/Pages/item.aspx?num=58253, accessed on July 14, 2020)

Clark, A., A. Ghosh and S. Hanes, 2018, “Inflation Expectations In Singapore:

A Behavioural Approach,” Macroeconomic Review, Vol 17:1, pp. 89-98.

Kouvavas, O., R. Trezzi, M. Eiglsperger, B. Goldhammer and E. Goncalves, 2020, “Consumption patterns and inflation measurement issues during the COVID-19 pandemic,” ECB Economic Bulletin, Issue 7/2020. (https://www.ecb.europa.eu/pub/economic-bulletin/html/eb202007.en.html#toc6, accessed on July 14, 2020)

Weber, M., F. D’Acunto, Y. Gorodnichenko and O. Coibion, 2022, “The Subjective Inflation Expectations of Households and Firms: Measurement, Determinants, and Implications,” Journal of Economic Perspectives, 36:3, pp. 157–184.

SINGAPORE, 20 April 2026 (Monday) - Singapore Management University’s Sim Kee Boon Institute for Financial Economics (SKBI), together with World Scientific Publishing, has released the Chinese version of ‘Sim Kee Boon: The Businessman Bureaucrat 沈基文:亦官亦商’, a biography of SKBI’s namesake.

The biography traces the life and legacy of Mr Sim Kee Boon, one of Singapore’s pioneer generation leaders who played a pivotal role in shaping the nation’s economic and institutional foundations. The biography was first published in English and was unveiled in 2022. This new Chinese edition seeks to extend these reflections to Chinese-speaking audiences, contributing to broader conversations on leadership and governance across the Chinese-speaking world.

Key roles in Singapore's pivotal nation-building moments

As a key civil servant hand-picked by the colonial government, Mr Sim participated in the merger talks with Malaysia. He also headed Intraco, the national trading company that was one of the drivers of the economy of a newly independent Singapore, and later became the Head of the Civil Service.

Mr Sim is acknowledged as a highly versatile and astute public officer who oversaw the development of Changi Airport, making it the world’s best airport in 2026, according to London-based research firm Skytrax. That Changi Airport has won this title 14 times since 2000 is no accident. The biography details, in Chapter 4, the drive and passion he felt to connect Singapore with the world seamlessly, with a clean, comfortable, and relaxing airport that would deliver baggage in a matter of minutes.

He also turned Keppel – a name closely tied with the maritime history of Singapore as a strategic port – into a diversified, visionary Singapore corporation. As co-chairman of the Singapore-Suzhou Industrial Township Development, a prominent government-to-government project between Singapore and China, from 1993 to 2000, Mr Sim worked with the Suzhou mayor on major agreements.

Co‑authored by Mr Sim’s granddaughter, Ms Leanne Sim, and biographer Ms Low Shi Ping, the 250-page book offers insight into the principles, values and leadership philosophy that guided Mr Sim’s career. More than an historical account, the biography offers reflections on decision-making and leadership in public service guided by strong values, and sheds light on the man behind the public figure, through the eyes of his granddaughter and on his life at home.

Impact beyond Singapore

Professor Hong Zhang, Director of SKBI and Keppel Professor in Financial Economics, said that as he was growing up in Suzhou, China, he witnessed the profound transformation brought about by the China–Singapore Suzhou Industrial Park.

He said: “Mr Sim’s leadership as Co-Chairman was instrumental to this achievement. The Chinese edition of this book stands as a fitting tribute to his enduring contributions to Singapore–China cooperation, alongside his many achievements in Singapore. His legacy continues to shape the mission of the Sim Kee Boon Institute for Financial Economics as we advance knowledge and foster international collaboration.”

‘A heart for the nation’

Ms Leanne Sim, Mr Sim’s granddaughter and co-author of the biography, said that the extensive interviews led her to see how her grandfather’s legacy has transcended his achievements. She said: “What strikes me most is this: people may forget what you say, but they will never forget how you made them feel. My grandfather embodied this truth. He had an unwavering heart for the nation, an unshakeable integrity, and an upright character that inspired those around him.”

To her, the book is more than a biography. “It is a values roadmap I hope to pass down to my children and future generations. It's a testament to how one person's commitment to purpose, principle, and people can shape an entire generation,” she said.

“The values that SKB stood for transcend culture, language, geography and time,” said Ms Low Shi Ping, the co-author. “I am glad that the Chinese-speaking world will now be able to learn about them through this book. His story deserves to be read by as many people as possible.”

The foreword is penned by Senior Minister Lee Hsien Loong, and the book comprises personal accounts of Mr Sim from 40 distinguished individuals, including Emeritus Senior Minister Goh Chok Tong and former Minister S. Dhanabalan. In 2022, it was launched by then Minister for Education and Minister-in-charge of the Public Service, Mr Chan Chun Sing.

The Chinese edition of Sim Kee Boon: The Businessman Bureaucrat ‘沈基文:亦官亦商’ is available at: Books Kinokuniya Singapore (Takashimaya S.C. & Online Store), Maha Yu Yi and Union Book Co Pte Ltd. The e-book is available here.

In a commentary, Dr Rajiv Lall, a Professorial Research Fellow at the SMU Sim Kee Boon Institute for Financial Economics and committee member at the Singapore Green Finance Centre, along with Vaibhav Pratap Singh, Executive Director of the Climate and Sustainability Initiative, highlight that India’s renewable energy goals face obstacles related to financing, grid integration, and storage. As India strives to reach 500GW by 2030, the challenge is moving from ambitious targets to providing reliable, financeable, and grid-connected renewable energy amid an increasingly complex energy landscape. With intricate tenders, changing storage strategies, and significant funding needs, a holistic strategy is essential. Additionally, expanding renewable energy will require addressing concerns over reliance on Chinese equipment.

*Please note that upon providing your consent to receive marketing communications from SMU SKBI, you may withdraw your consent, at any point in time, by sending your request to skbi_enquiries [at] smu.edu.sg (subject: Withdrawal%20consent%20to%20receive%20marketing%20communications%20from%20SMU) (skbi_enquiries[at]smu[dot]edu[dot]sg). Upon receipt of your withdrawal request, you will cease receiving any marketing communications from SMU SKBI, within 30 (thirty) days of such a request.