These are the research findings of the 31st round of quarterly release for the DBS-SKBI Singapore Index of Inflation Expectations (SInDEx) Survey at the Sim Kee Boon Institute for Financial Economics (SKBI), Singapore Management University (SMU).

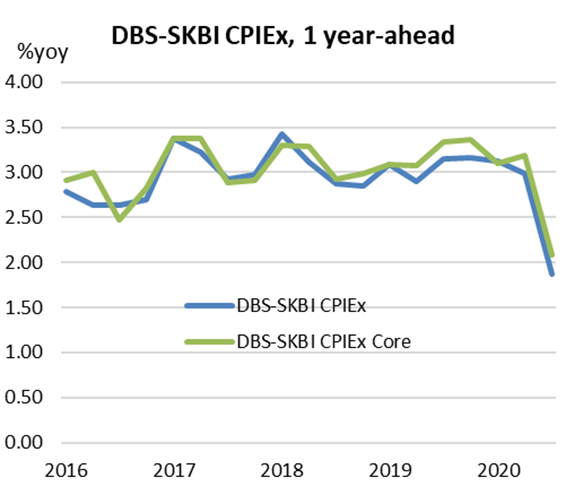

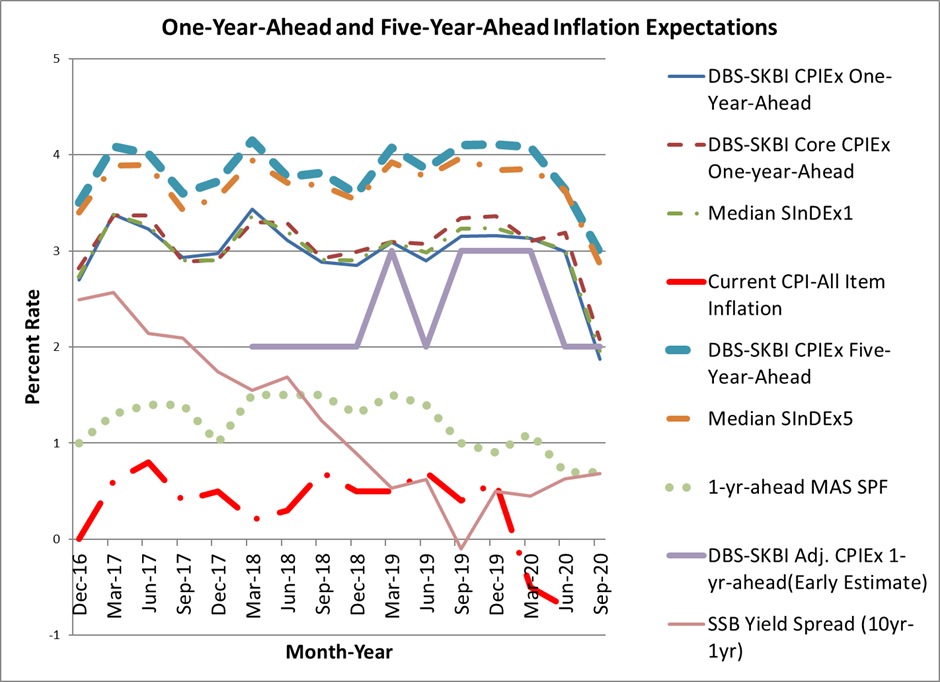

Singaporeans’ One-year-Ahead headline inflation expectations polled at 3.1% in March 2019. The reading compares to 2.9% polled in December 2018, and the first quarter long-term (2012-18) average of 3.4%.

DBS-SKBI SInDEx survey was augmented in June 2018, based on a joint research study conducted by SMU researchers in collaboration with the Monetary Authority of Singapore (MAS) and the Behavioral Insights Team, where respondents were polled about their perceptions of components of the Consumers Price Index (CPI) and adjusted for possible behavioral biases prevalent in online surveys.

Based on the recommendations of that study the research team had, in March 2019 polled the one-year-ahead inflation expectations of all of the components of CPI-All Items inflation. Compared to December 2018, the March 2019 survey revealed inflation expectations across all categories have moved up quarter on quarter, although without the same quarterly benchmark we were not able to conclude if the uptick is a peculiarity or a natural quarterly seasonality of these indices.

The overall CPIEx Inflation Expectations, after adjusting for potential behavioral biases and re-combining across components, was at 3.07% in March 2019, similar to the CPIEx headline inflation rates polled. This also suggests that Singaporeans’ inflation expectations are well-grounded from both the aggregated and the components-wise comparisons.

Excluding accommodation and private road transportation related costs, the One-year-Ahead Core CPIEx inflation expectations was recorded at 3.1% in March 2019 (compared to 3.0% reported in the December 2018 survey). For a subgroup of the population who own their accommodation and use public transport, the One-year-Ahead CPIEx core inflation expectations inched up to 3.0% from 2.9% in December 2018. This subgroup’s expectations of core inflation closely resembles the Singapore Core Inflation Expectations, as unlike the general population they are not exposed to private road transportation or accommodation expenses.

DBS Chief Economist and Managing Director of Group Research, Dr. Taimur Baig commented, “amid slowing growth and uncertainty about the global demand outlook, inflation expectations appear broadly stable. As commodity prices firm and expectations of global demand revival (led by China) sets in, conditions for a mild increase in expectations are in place.”

For the longer horizon, the Five-year-Ahead CPIEx inflation expectations in the March 2019 survey moved up to 4.1% from 3.6% in December 2018. The current polled number is lower than the long-term (from 2012-18) average of 4.2%.

The Five-year-Ahead DBS-SMU CPIEx core inflation expectations (excluding accommodation and private road transportation related costs) pared to 3.8% in March 2019 from 3.5% in December 2018. Overall, the composite Five-year-Ahead SInDEx5 increased to 3.9% in March 2019 from 3.5% in December 2018, still polling lower than its historical average of 4.1%.

SMU Assistant Professor of Finance and Principal Investigator of the DBS-SKBI SInDEx Project, Aurobindo Ghosh observed, “There have been several factors that might have led to an overall downbeat forecast by IMF World Economic Outlook in April 2019 for global growth despite significant green shoots such as the possible resolution for the Sino-US trade dispute and the breakthrough in extending of Article 50 to prevent a hard Brexit. This sentiment of a moderation in global growth has also been communicated by the US Federal Reserve Board as a primary driver opting for halting rate hikes and preferring patience in a short run and a data driven outlook for the longer run monetary policy with persistently low inflation. We have observed that the impact of this declining growth and possible downturn is also felt in the decline in the yield spread of Singapore government bonds (difference between the yield of 10-year and 1-year bonds).”

”Overall inflation has been largely benign since the tightening of the monetary policy in previous two semiannual policy reviews by MAS in 2018. We do however observe some possible pass-through of domestic price pressures from the quarterly DBS-SKBI SInDEx survey that yields the CPIEx along with a dashboard of other measures of inflation expectations, for both behaviorally adjusted and unadjusted series. There are often counterbalancing pressures with varying outcomes such as slight increase in global oil prices although deregulation in the retail electricity market has a downward pressure on electricity prices, moderation in decline in accommodation and private road transportation prices despite increasing wages in the domestic labor market. Unsurprisingly, in their current semiannual review in April 2019 the policymakers held their monetary policy unchanged.” Prof. Ghosh added.