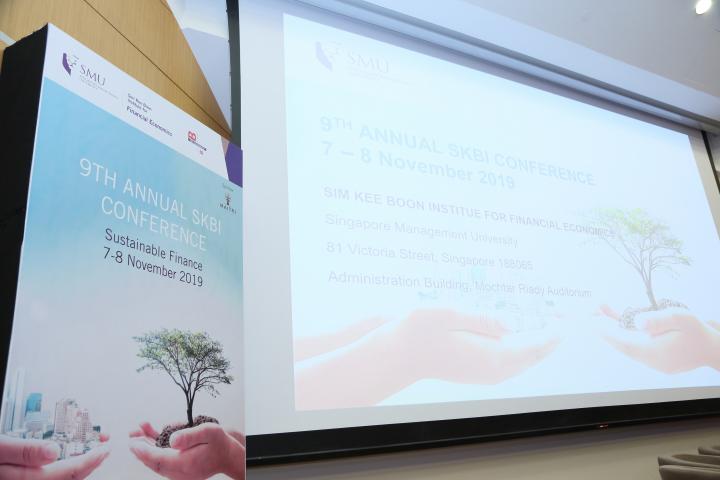

Recognising the growing interest among finance practitioners and policymakers on Sustainable Finance, the Sim Kee Boon Institute for Financial Economics (SKBI) at Singapore Management University, in partnership with the TBLI Group of the Netherlands, organised the 9th Annual SKBI conference on "Sustainable Finance" on 7-8 November 2019.

The 1.5-day event brought together 200 local and overseas participants from the finance and banking industry, government agencies, businesses and academia to discuss and share the latest developments and insights in the area of sustainable finance.

In their welcome speeches, Dean of SMU Lee Kong Chian School of Business Professor Gerard George, Director of SKBI Professor David Fernandez, and Mr Robert Rubinstein, Chairman of TBLI Group, shared about the objectives and programme of the conference.

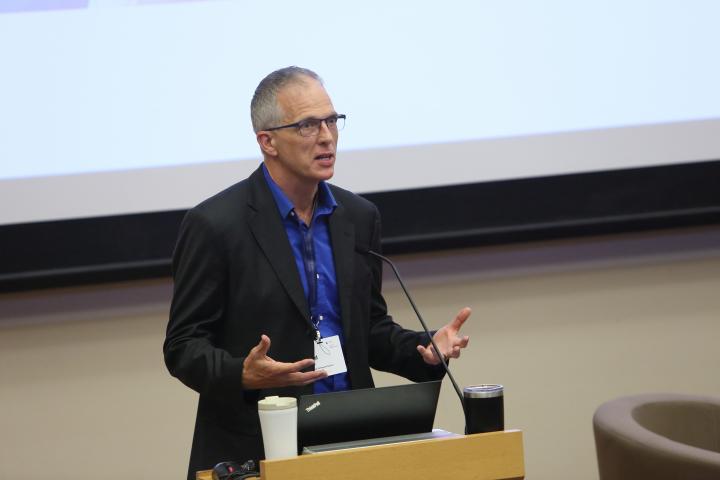

Professor Brad M. Barber

Professor Brad M. Barber, Gallagher Professor of Finance, Graduate School of Management, University of California at Davis, USA, kicked off the proceedings on the first day with his keynote speech on ‘What academic research shows about sustainable finance’. He shared the findings of a research in which his co-authors and he sought to understand whether investors are willing to accept lower financial returns for nonpecuniary benefits of intentional impact investing.

They documented that financial returns earned by impact funds are 4.7% lower than those earned by traditional venture capital funds. To examine whether investors in impact funds willingly trade off expected financial returns at the time of investment decisions, they used a pricing framework of willingness to pay (WTP) for impact, and found that investors accept 2.5-3.7% lower IRRs for impact funds. The research found that development organisations, banks, insurance companies, and public pensions exhibit reliably positive willingness to pay for impact.

As for what attributes of investors affect investors’ willingness to pay for impact, the research found that investors with organisational missions have high WTP. In addition, investors facing political and/or regulatory pressure and those benefiting from political or local goodwill exhibit a higher willingness to pay for impact. In contrast, those subject to legal restrictions (e.g., Employee Retirement Income Security Act) exhibit low WTP for impact.

Dr Priscilla Lu

In the second keynote address, Dr Priscilla Lu, Head of Sustainable Investments, Alternatives For DWS Asia, DWS, Hong Kong, who is also an SKBI Advisory Board Member, spoke on “Smart Cities and Sustainable Finance”.

Dr Lu shared that news report have shown that China’s urbanisation rate was at 58.5% as of 2017 and is expected to reach 70% by 2035. According to the United Nations, global urbanisation rate was at 55% in 2015 and is expected to reach 68% by 2050. Such rapid urbanisation is creating a lot of stress on cities to be able to manage the increasing scale of challenges such as traffic congestion, security and garbage collection. To respond to these challenges and provide the services required by urban dwellers, cities will have to leverage smart technologies.

A study has forecasted the smart cities market size to grow from US$308.0 billion in 2018 to US$717.2 billion by 2023, at a Compound Annual Growth Rate of 18.4%. Another study indicated that global Smart City revenue will reach US$88.7 billion by 2025. A report also informed that worldwide spending on the technologies that enable Smart Cities is forecast to reach US$80 billion in 2018. Over five years, that total will reach US$135 billion by 2021.

Factors such as a need for public safety and communication infrastructure, citizen empowerment and engagement, and increased adoption rate of advanced technologies, are driving the smart cities market. Increased environmental concerns, growing demand for advanced technologies such as loT and 5G, and developing economies are generating a number of opportunities for smart cities market.

Mr Mikkel Larsen

The keynote speaker for Day 2 of the conference was Mr Mikkel Larsen, Chief Sustainability Officer of DBS who spoke on “Financing Solutions to Societal Problems at Scale – A Case for Impact Measurement”. He opined that the key to impact investing and impact measurement is data, in particular, social and environmental data, so that capital is not misallocated based on wrong or incomplete understanding of a project’s impact.

Such data must be captured in an affordable way, are free, credible, meaningful, complete and comparable. The resultant digital finance will help promote financial inclusion so that 1.7 billion people (more than 25 percent) in the world who currently do not have access to basic banking products will be served. It will also help encourage sustainable finance where capital is channelled to where it can do the most good and least harm. Digital finance can also help to drive sustainable practices by using technology to create awareness and drive consumer behaviour through digital means.

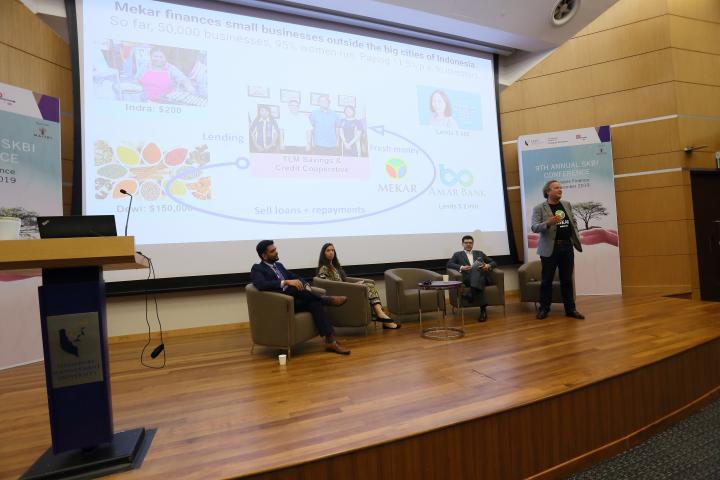

In addition to the keynote speeches, there were two roundtable discussions on ‘Engaging Family Offices on Impact Investing’ and ‘Climate Strategy at Scale’, as well as numerous workshops on a range of topics, including ‘Gender-Smart Impact Investing’, ‘Green Infrastructure’, Impact Investing in Greater China’, and ‘Impact Measurement’.